Income tax can feel complicated because the rules combine definitions (what counts as income), calculations (how taxable income is determined), and policy design (progressive brackets, allowances, deductions, credits). The good news is that most systems follow a fairly consistent structure. Once you understand the moving parts, you can usually read a payslip, estimate your liability, and explain why two people with the same salary may pay different amounts.

This guide explains:

- Tax brackets and how progressive tax works

- The difference between marginal and effective tax rates

- Deductions and how they reduce taxable income

- A clear, repeatable method to calculate taxable income and estimated tax

- Worked examples and practical tables you can reuse

Note: Tax laws vary by jurisdiction, and the definitions below are “typical” rather than universal. Always verify with your local tax authority or a qualified professional for your specific situation.

1) What Income Tax Is

Income tax is a levy on income earned by individuals (and often separate rules for businesses). It is usually assessed over a defined period (often a tax year). Depending on where you live, it may apply at multiple levels (national, regional, local), and the rates may depend on filing status, dependents, residency, and the type of income.

What most people want to know is simple:

- How much will I owe?

- Why is it that amount?

- How do deductions change it?

- What does my tax rate actually mean?

Those questions require one foundational distinction.

2) Gross Income vs Taxable Income

Many people assume tax is calculated on their salary. Often it is not. Tax is typically calculated on taxable income, which may be lower than gross income due to exclusions, adjustments, and deductions.

Typical income tax flow (high-level)

- Gross income (salary + other income)

- Minus certain exclusions (income not taxed at all)

- Equals adjusted income (or similar concept)

- Minus deductions (expenses/allowances that reduce taxable income)

- Equals taxable income

- Apply tax brackets to compute preliminary tax

- Subtract tax credits (if applicable)

- Equals final tax owed (or refund if withholding was higher)

Not every system uses the same terminology, but the pipeline is broadly similar.

3) Tax Brackets: How Progressive Tax Actually Works

A progressive tax system applies higher rates to higher slices of income. The key idea is that you do not pay the top rate on all your income. You pay different rates on different portions, depending on bracket thresholds.

The bracket concept

Imagine brackets as “layers” of income. Each layer has:

- A range (e.g., 0–20,000)

- A rate (e.g., 10%)

You pay that rate only on income within that range.

Example bracket schedule (illustrative)

Below is a fictional, easy-to-follow bracket system used for demonstrations in this article:

| Taxable Income Slice | Rate |

|---|---|

| 0 – 20,000 | 10% |

| 20,001 – 50,000 | 15% |

| 50,001 – 100,000 | 20% |

| 100,001 – 200,000 | 25% |

| 200,001+ | 30% |

4) Marginal vs Effective Tax Rate (The Most Misunderstood Topic)

Marginal tax rate

Your marginal tax rate is the rate applied to your next unit of taxable income (often the highest bracket you reach). It answers:

- “If I earn 1 more, how much extra tax will I pay?”

Effective tax rate

Your effective tax rate is your total tax divided by your total taxable income. It answers:

- “Overall, what percentage of my taxable income went to tax?”

Formulas

Marginal_rate = rate_of_highest_bracket_reached

Effective_rate = Total_tax / Taxable_income

Why the difference matters

Two people can both be “in the 20% bracket,” but their effective rates may differ due to deductions, credits, and how much income falls into lower brackets.

5) Deductions: What They Are and Why They Matter

A deduction reduces taxable income. That means it reduces the portion of income subject to tax.

Deductions do not reduce tax 1-for-1

A common mistake is thinking “a 1,000 deduction saves 1,000 in tax.” It does not. The tax savings depends on your marginal rate.

Tax_savings_from_deduction ≈ Deduction_amount * Marginal_rate

Example: If your marginal rate is 20%, a 1,000 deduction typically reduces tax by about 200.

Common types of deductions (varies by jurisdiction)

- Contributions to qualifying retirement/pension plans

- Certain education-related expenses

- Qualified interest expenses (limited and conditional)

- Charitable contributions (often with restrictions)

- Work-related expenses (sometimes restricted, sometimes disallowed)

- Medical expenses above a threshold (in some systems)

Standard deduction vs itemized deductions (or allowance vs detailed claims)

Many systems give taxpayers a choice between:

- A fixed deduction/allowance (simple)

- Itemized/detailed deductions based on actual eligible expenses (more complex)

You typically choose whichever is larger (if allowed), because it lowers taxable income more.

6) How Taxable Income Is Calculated (Step-by-Step)

Here is a practical template you can use:

Step 1: Add up gross income

This may include:

- Employment income (salary/wages/bonuses)

- Self-employment income (net of business expenses)

- Investment income (interest/dividends)

- Rental income (net of eligible expenses)

- Certain benefits (depending on local rules)

Gross_income = Salary + Bonus + Other_income

Step 2: Subtract adjustments (if applicable)

Some systems allow “above-the-line” adjustments that reduce income before deductions.

Adjusted_income = Gross_income - Adjustments

Step 3: Subtract deductions to arrive at taxable income

Taxable_income = Adjusted_income - Deductions

Step 4: Apply tax brackets to taxable income

Compute tax by slicing income into bracket ranges:

Total_tax = Σ (Income_in_bracket_i * Rate_i)

Step 5: Subtract credits (if applicable)

Credits reduce tax directly.

Final_tax = Total_tax - Credits

Step 6: Compare to withholding or prepayments

If tax has already been withheld from wages or paid in instalments:

Balance_due_or_refund = Final_tax - Withholding

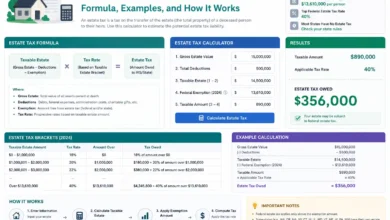

7) Worked Example: Brackets in Action

Using the illustrative bracket schedule earlier, suppose a person has:

- Gross income: 72,000

- Adjustments: 2,000

- Deductions: 10,000

Step A: Compute taxable income

Adjusted_income = 72,000 - 2,000 = 70,000

Taxable_income = 70,000 - 10,000 = 60,000

Step B: Apply brackets to 60,000

Break 60,000 into slices:

- 0–20,000 at 10% → 20,000 * 0.10 = 2,000

- 20,001–50,000 at 15% → 30,000 * 0.15 = 4,500

- 50,001–60,000 at 20% → 10,000 * 0.20 = 2,000

Total_tax = 2,000 + 4,500 + 2,000 = 8,500

Step C: Marginal vs effective rate

- Marginal rate: 20% (highest bracket reached)

- Effective rate:

Effective_rate = 8,500 / 60,000 = 0.1417 ≈ 14.17%

Even though the person is “in the 20% bracket,” their overall tax on taxable income is about 14.17%.

8) What a Deduction Is “Worth” at Different Marginal Rates

This table shows approximate tax savings from a deduction, depending on marginal rate:

| Deduction Amount | 10% Marginal | 15% Marginal | 20% Marginal | 25% Marginal | 30% Marginal |

|---|---|---|---|---|---|

| 500 | 50 | 75 | 100 | 125 | 150 |

| 1,000 | 100 | 150 | 200 | 250 | 300 |

| 5,000 | 500 | 750 | 1,000 | 1,250 | 1,500 |

| 10,000 | 1,000 | 1,500 | 2,000 | 2,500 | 3,000 |

This is why higher-income taxpayers (who face higher marginal rates) often experience larger tax savings from the same deduction amount—subject to eligibility limits.

9) Deductions vs Credits (Do Not Confuse These)

While deductions reduce taxable income, credits reduce tax owed.

Deductions

Taxable_income = Income - Deductions

Credits

Final_tax = Computed_tax - Credits

A 1,000 credit often reduces tax by 1,000 (subject to rules). A 1,000 deduction reduces tax by about 1,000 * marginal_rate.

Quick comparison table

| Feature | Deduction | Credit |

|---|---|---|

| Reduces | Taxable income | Tax owed |

| Value depends on | Marginal rate | Credit rules (often 1-for-1) |

| Typical examples | retirement contributions, eligible expenses | family credits, education credits, low-income credits |

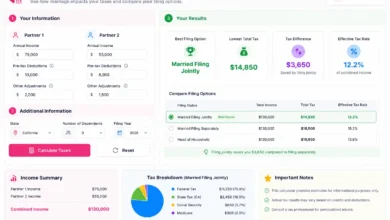

10) Example: Two People, Same Income, Different Taxes

Let’s say both people earn the same gross income: 80,000. Same bracket schedule. But they have different deductions.

Person A

- Adjustments: 0

- Deductions: 5,000

- Taxable income: 75,000

Tax on 75,000:

- 20,000 at 10% = 2,000

- 30,000 at 15% = 4,500

- 25,000 at 20% = 5,000

Total tax = 11,500

Effective rate:

11,500 / 75,000 ≈ 15.33%

Person B

- Adjustments: 0

- Deductions: 20,000

- Taxable income: 60,000

From earlier example method, tax on 60,000 = 8,500

Effective rate:

8,500 / 60,000 ≈ 14.17%

Same gross income, different taxable income, different tax outcome.

11) How Withholding Fits In (Why You Might Owe or Get a Refund)

Many employees have taxes withheld from each pay period. Withholding is not the final calculation—it is a prepayment.

At filing/assessment time:

- If withholding > final tax → refund/credit

- If withholding < final tax → balance due

Important: a refund does not automatically mean you “paid less tax.” It often means you overpaid during the year.

12) Common Pitfalls That Create Confusion

Pitfall 1: “If I move into a higher bracket, I lose money”

Not in a typical progressive bracket system. Only the income above the threshold is taxed at the higher rate.

Pitfall 2: Confusing marginal and effective rates

Your marginal rate is about the next unit of income; your effective rate is the overall average.

Pitfall 3: Treating deductions as guaranteed tax savings

A deduction only helps if it is eligible and properly documented (where required), and its value depends on marginal rate.

Pitfall 4: Ignoring other taxes

Many jurisdictions also have payroll contributions, social insurance, or local levies that are separate from income tax.

13) Practical Estimation Method (A Simple Checklist)

If you want a clean estimate without getting lost in details:

- Estimate gross income (all sources)

- Subtract known adjustments (if any)

- Choose the larger of fixed allowance vs itemized deductions (if your system allows)

- Compute taxable income

- Apply brackets to compute preliminary tax

- Subtract eligible credits

- Compare to withholding/prepayments

You can do most of this in a basic spreadsheet.

FAQs

1) What are tax brackets?

Tax brackets are income ranges taxed at specific rates. In progressive systems, higher portions of income are taxed at higher rates.

2) What is the marginal tax rate?

Your marginal tax rate is the rate applied to your next unit of taxable income, usually the highest bracket you reach.

3) What is the effective tax rate?

Your effective tax rate is total tax divided by taxable income:

Effective_rate = Total_tax / Taxable_income

4) Do I pay my top bracket rate on all my income?

Typically, no. You pay different rates on different slices of income. Only income within the top bracket range is taxed at the top rate.

5) What’s the difference between gross income and taxable income?

Gross income is your total income before reductions. Taxable income is what remains after adjustments and deductions:

Taxable_income = Income - Adjustments - Deductions

6) How do deductions reduce my taxes?

Deductions reduce taxable income. The tax benefit depends on your marginal rate:

Tax_savings ≈ Deduction * Marginal_rate

7) Are deductions the same as credits?

No. Deductions reduce taxable income; credits reduce tax owed directly:

Final_tax = Computed_tax - Credits

8) Why did I get a refund?

Often because more tax was withheld during the year than your final calculated tax. A refund is commonly an overpayment being returned.

9) Why can two people with the same salary owe different taxes?

They may have different deductions, credits, filing status rules, dependents, residency status, or different types of income taxed under different regimes.

10) What is the best way to avoid surprises at year-end?

Track taxable income, understand what affects deductions and credits, and align withholding/prepayments with your expected final tax.