An interest calculator estimates how much interest you will earn (on savings/investments) or pay (on loans/credit) over a specific period. The result depends on three core variables—principal, interest rate, and time—plus the method used to apply interest: simple interest, compound interest, or amortized payments.

This article explains how interest calculators work, the formulas they use, and practical examples you can verify by hand. Also, Read – Loan Calculator: Formula, Examples, and How It Works

What an Interest Calculator Does

Depending on the calculator type, it can compute:

- Interest earned or paid over a period

- Ending balance after interest is applied

- Effective annual rate (how compounding changes real cost/return)

- Payment amount for installment loans (if applicable)

- Amortization breakdown (interest vs principal over time)

- Impact of compounding frequency (daily vs monthly vs annually)

- Impact of deposits/withdrawals (regular contributions)

Most “interest calculators” fall into one of these categories:

- Simple interest calculator

- Compound interest calculator

- Loan/credit interest calculator (amortized payment + interest schedule)

Key Inputs and Definitions

Principal (P)

The starting amount of money.

- Savings: initial deposit

- Loans: amount borrowed

Interest rate (R or r)

The percentage charged or earned, typically expressed annually.

- APR is common for loans

- APY or EAR may be used for savings to reflect compounding

Time (t)

How long the money accrues interest.

- in years, months, or days depending on the formula

Compounding frequency (m)

How often interest is applied.

- annually (1), monthly (12), daily (365), etc.

Payment (PMT)

For loans, the fixed periodic amount you pay.

Simple Interest Calculator

Simple interest applies interest only to the original principal (not to accumulated interest). It is common in short-term notes and some basic lending arrangements, and it’s useful as a baseline for comparison. Also, Read – Auto Loan Calculator: Formula, Examples, and How It Works

Simple interest formula

I = P * r * t

A = P + I

Where:

I= interestA= total amount (ending balance)P= principalr= annual interest rate (decimal)t= time in years

Example 1: Simple interest on savings

Assume:

- P = 5,000

- r = 8% = 0.08

- t = 3 years

I = 5000 * 0.08 * 3 = 1200

A = 5000 + 1200 = 6200

Result: Interest = 1,200, Ending balance = 6,200

Example 2: Simple interest on a short loan

Assume:

- P = 2,000

- r = 12% = 0.12

- t = 9 months = 0.75 years

I = 2000 * 0.12 * 0.75 = 180

A = 2000 + 180 = 2180

Result: Interest = 180, Total repayment = 2,180

Compound Interest Calculator

Compound interest applies interest to both principal and accumulated interest. This is the standard for most savings products, investments, and many loan interest calculations (though loans usually involve payments too). Also, Read – Compound Interest Explained: APY, Compounding Frequency, and

Compound interest formula (no contributions)

A = P * (1 + r/m)^(m*t)

I = A - P

Where:

m= compounding periods per year- other variables are as defined above

Example 3: Compounded monthly

Assume:

- P = 10,000

- r = 6% = 0.06

- m = 12

- t = 5 years

A = 10000 * (1 + 0.06/12)^(12*5)

A = 10000 * (1.005)^60

Approximate:

(1.005)^60 ≈ 1.34885

A ≈ 10000 * 1.34885 = 13488.50

I ≈ 3488.50

Result: Ending balance ≈ 13,488.50; Interest ≈ 3,488.50

Example 4: Daily vs monthly compounding (same nominal rate)

Assume:

- P = 10,000

- r = 6%

- t = 5 years

Monthly compounding:

A_monthly = 10000 * (1 + 0.06/12)^(60) ≈ 13,488.50

Daily compounding:

A_daily = 10000 * (1 + 0.06/365)^(365*5)

Daily compounding yields a slightly higher result because interest is applied more frequently. The difference is usually modest at typical consumer rates but becomes meaningful over long horizons or larger balances. Also, Read – Investment Growth Explained: Compounding With Clear Examples

Effective Annual Rate (EAR) and APY

Interest calculators often show an “effective” rate, because compounding changes the real annual outcome versus the nominal rate.

Effective annual rate formula

EAR = (1 + r/m)^m - 1

Example 5: 6% nominal, compounded monthly

EAR = (1 + 0.06/12)^12 - 1

EAR = (1.005)^12 - 1

Approximate:

(1.005)^12 ≈ 1.06168

So:

EAR ≈ 0.06168 = 6.168%

Meaning: A “6% rate compounded monthly” effectively behaves like about 6.168% per year.

Compound Interest with Regular Contributions

Many interest calculators let you include monthly deposits (or payments). This is common for savings and retirement projections.

There are two standard cases:

- contributions at the end of each period (ordinary annuity)

- contributions at the beginning (annuity due)

Future value with end-of-period contributions (ordinary annuity)

FV = P*(1 + r/m)^(m*t) + PMT * [((1 + r/m)^(m*t) - 1) / (r/m)]

Where:

PMT= contribution each period (aligned with m)r/m= periodic rate

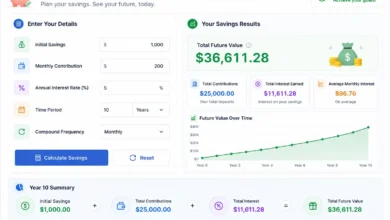

Example 6: Monthly saving with monthly compounding

Assume:

- P = 2,000 initial

- PMT = 200 per month

- r = 6% nominal

- m = 12

- t = 5 years (60 months)

Periodic rate:

i = 0.06/12 = 0.005- growth factor:

(1.005)^60 ≈ 1.34885

Compute:

FV = 2000*(1.34885) + 200 * [(1.34885 - 1)/0.005]

FV = 2697.70 + 200 * [0.34885/0.005]

FV = 2697.70 + 200 * 69.77

FV = 2697.70 + 13,954.00

FV ≈ 16,651.70

Total contributions = 2,000 + (200*60) = 14,000

Interest earned ≈ 16,651.70 − 14,000 = 2,651.70

Loan Interest Calculator (Amortized Loans)

For car loans, personal loans, and many mortgages, the interest calculation is tied to fixed payments. Here the question is not just “how much interest accrues,” but “what payment clears the balance over time.”

Monthly payment formula (amortizing loan)

PMT = P * [ i * (1 + i)^n ] / [ (1 + i)^n - 1 ]

Where:

PMT= periodic paymentP= loan principali= periodic interest rate (APR/12 for monthly)n= number of payments

Interest and principal split each month

Interest_k = Balance_(k-1) * i

Principal_k = PMT - Interest_k

Balance_k = Balance_(k-1) - Principal_k

Example 7: Installment loan interest over time

Assume:

- P = 20,000

- APR = 9% → i = 0.09/12 = 0.0075

- n = 48 months

Payment:

PMT = 20000 * [ 0.0075*(1.0075)^48 ] / [ (1.0075)^48 - 1 ]

A calculator will output the precise monthly payment. The important takeaway is how interest behaves:

- early months: interest portion is higher (balance is highest)

- later months: principal portion rises as balance falls

This is why paying extra early saves more interest than paying extra late.

Daily Interest Calculations (Common in Some Credit Products)

Some calculators estimate interest using daily accrual:

Daily simple interest (common structure)

DailyRate = APR / 365

Interest = Balance * DailyRate * Days

Example 8: Daily interest on a balance

Assume:

- Balance = 3,000

- APR = 18% → 0.18

- Days = 20

DailyRate = 0.18/365 ≈ 0.00049315

Interest ≈ 3000 * 0.00049315 * 20 ≈ 29.59

Result: about 29.59 interest for 20 days (approx.)

What Changes Interest the Most (In Real Life)

When you adjust inputs in an interest calculator, the biggest drivers are:

- Rate (APR/APY/EAR)

- small changes matter over long time periods

- Time

- interest accelerates with compounding over longer horizons

- Compounding frequency

- more frequent compounding increases effective returns/costs

- Principal

- interest scales with balance

- Payments/contributions timing

- earlier contributions earn interest longer; extra loan payments reduce interest sooner

Common Calculator Mistakes

Mixing APR and APY

APR is typically a nominal rate used for cost; APY/EAR reflect compounding. Make sure you compare like-for-like.

Using months in a “years” formula without converting

If a formula assumes t is in years, convert months to years:

t = months / 12

Forgetting compounding frequency

“6% compounded monthly” and “6% compounded annually” will not produce the same ending balance.

Treating loan interest like compound savings

Loans with fixed payments require amortization math, not just compound growth formulas.

How to Choose the Right Interest Calculator

Use a:

- Simple interest calculator if interest is only on principal and there are no compounding effects.

- Compound interest calculator for savings/investments (especially with compounding and contributions).

- Loan/amortization calculator for installment loans with fixed payments.

- Daily interest calculator for products that accrue interest day-by-day.

FAQs

Is compound interest always better than simple interest?

For savings, compounding increases earnings compared to simple interest. For debt, compounding increases cost. “Better” depends on whether you are earning or paying.

Why does interest feel slow at first on savings but high on loans?

Savings growth may look gradual early because the base is small. Loans feel interest-heavy early because the balance is large and payments are structured to be level while interest declines over time.

Does a higher compounding frequency always matter?

Yes, but the difference can be small for typical rates and short durations. Over long time periods or high balances, it becomes more noticeable.

How accurate are online interest calculators?

They are accurate if the assumptions match your product terms: rate, compounding method, payment schedule, fees, and timing.

How do extra payments affect loan interest?

Extra payments reduce principal faster, which reduces interest and can shorten the payoff period—especially if applied early.

Summary

An interest calculator applies standard formulas based on how interest is defined:

- Simple interest:

I = P * r * t A = P + I - Compound interest:

A = P * (1 + r/m)^(m*t) I = A - P - Amortized loan payment:

PMT = P * [ i * (1 + i)^n ] / [ (1 + i)^n - 1 ]

The most important step is choosing the correct model (simple, compound, amortized, or daily accrual) and ensuring your inputs match the way your bank or lender applies interest.