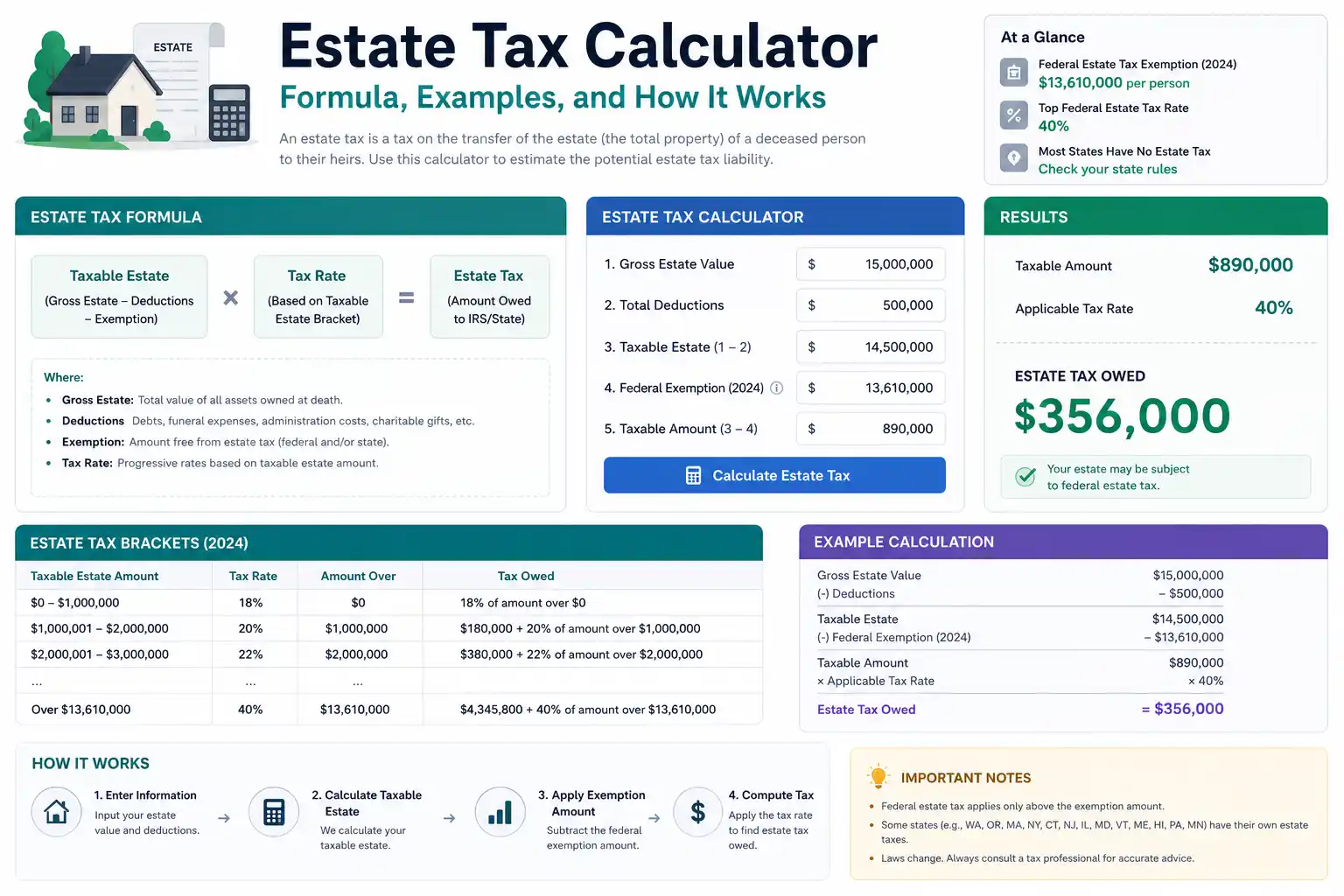

What Is an Estate Tax Calculator?

An estate tax calculator is a financial and legal planning tool that estimates the federal — and where applicable, state — estate tax owed on the transfer of a deceased person’s assets to their heirs. It takes the gross value of an estate, subtracts allowable deductions and the applicable exemption amount, applies the estate tax rate schedule to the resulting taxable estate, and produces an estimated tax liability.

Estate taxes are sometimes called the “death tax” — a loaded political term, but one that accurately describes the basic mechanism: a tax levied on the right to transfer accumulated wealth at death. They are among the most misunderstood taxes in the U.S. code, partly because most Americans will never owe federal estate tax (the exemption threshold is very high), and partly because the rules have changed dramatically over the past two decades and are scheduled to change again significantly in 2026.

Understanding how an estate tax calculator works matters not only for wealthy individuals whose estates may exceed the exemption but also for financial planners, estate attorneys, accountants, and family members trying to understand the tax consequences of an inheritance — or plan an estate to minimize them.

Who Actually Owes Federal Estate Tax?

The federal estate tax applies only to estates whose gross value exceeds the federal estate tax exemption — the amount that can be transferred tax-free at death.

For 2024, the federal exemption is $13.61 million per individual ($27.22 million for a married couple using portability). This means the overwhelming majority of American estates owe zero federal estate tax. According to IRS data, fewer than 0.1% of deaths in recent years resulted in any federal estate tax liability.

However, the current high exemption is scheduled to sunset on January 1, 2026, reverting to approximately $7 million per individual (the pre-TCJA level, adjusted for inflation) unless Congress acts to extend or modify it. This scheduled change — the most significant estate tax development in years — makes estate planning and estate tax calculation significantly more urgent for individuals with estates in the $7–$14 million range.

The Federal Estate Tax Formula

The estate tax calculation follows a structured sequence:

Step 1: Calculate the Gross Estate

Gross Estate = Fair Market Value of All Assets Owned at Death

The gross estate includes:

- Real estate (at fair market value, not purchase price)

- Bank accounts, investment accounts, retirement accounts

- Life insurance proceeds (if the decedent owned the policy)

- Business interests and partnerships

- Personal property (vehicles, jewelry, art, collectibles)

- Certain gifts made within 3 years of death

- Revocable trust assets

Step 2: Calculate the Adjusted Gross Estate

Adjusted Gross Estate = Gross Estate − Allowable Deductions

Allowable deductions include:

- Funeral expenses

- Estate administration expenses (attorney fees, executor fees, court costs)

- Debts of the decedent (mortgages, credit card debt, loans)

- Casualty and theft losses during estate administration

- The unlimited marital deduction (assets left to a U.S. citizen spouse are fully deductible — zero estate tax owed)

- Charitable deductions (assets left to qualifying charities are fully deductible)

Step 3: Calculate the Taxable Estate

Taxable Estate = Adjusted Gross Estate − Applicable Exemption Amount

For 2024: Applicable Exemption = $13,610,000 per individual

If the Taxable Estate is zero or negative, no federal estate tax is owed.

Step 4: Apply the Estate Tax Rate Schedule

Estate Tax = Tax on Taxable Estate (per IRS rate schedule)

Step 5: Apply Credits

Net Estate Tax = Estate Tax − Unified Credit − State Death Tax Credit (if applicable)

The unified credit is the tax credit equivalent of the exemption amount. In practice, Steps 3 and 5 are combined — the exemption is simply subtracted before rates are applied.

The Federal Estate Tax Rate Schedule

The federal estate tax is progressive — higher portions of the taxable estate are taxed at higher rates. The top marginal rate is 40%, but the effective rate on the entire taxable estate is always lower because only the amount above each threshold is taxed at that tier’s rate.

2024 Federal Estate Tax Rate Schedule

| Taxable Estate Value | Tax Rate | Cumulative Tax at Top |

|---|---|---|

| $0 – $10,000 | 18% | $1,800 |

| $10,001 – $20,000 | 20% | $3,800 |

| $20,001 – $40,000 | 22% | $8,200 |

| $40,001 – $60,000 | 24% | $13,000 |

| $60,001 – $80,000 | 26% | $18,200 |

| $80,001 – $100,000 | 28% | $23,800 |

| $100,001 – $150,000 | 30% | $38,800 |

| $150,001 – $250,000 | 32% | $70,800 |

| $250,001 – $500,000 | 34% | $155,800 |

| $500,001 – $750,000 | 37% | $248,300 |

| $750,001 – $1,000,000 | 39% | $345,800 |

| Over $1,000,000 | 40% | — |

In practice, because the exemption absorbs the first $13.61 million, only the amount above $13.61 million is subject to these rates — and realistically, all of that excess will fall into the 40% bracket for estates large enough to owe any tax at all.

Simplified effective formula for most taxable estates:

Federal Estate Tax ≈ (Gross Estate − Deductions − $13,610,000) × 40%

This approximation is accurate for estates where the entire taxable portion exceeds $1,000,000 above the exemption — which is virtually all estates that owe any federal estate tax.

Step-by-Step Estate Tax Calculation Examples

Example 1: Estate Below the Exemption — No Tax Owed

Deceased: Helen Marsh Gross Estate: $4,200,000

- Primary residence: $850,000

- Investment accounts: $2,100,000

- Retirement accounts (IRA): $900,000

- Life insurance (owned by Helen): $250,000

- Personal property and vehicles: $100,000

Deductions:

- Funeral expenses: $18,000

- Estate administration: $42,000

- Outstanding mortgage: $120,000

- Credit card debt: $8,000

- Total deductions: $188,000

Adjusted Gross Estate = $4,200,000 − $188,000 = $4,012,000

Taxable Estate = $4,012,000 − $13,610,000 = −$9,598,000

Federal Estate Tax: $0

Helen’s estate is well below the 2024 federal exemption. No federal estate tax is owed, and her heirs receive the full estate (less income taxes on inherited IRA distributions, which are a separate matter from estate tax).

Example 2: Estate Above the Exemption — Tax Owed

Deceased: Richard Calloway Gross Estate: $18,500,000

- Business interest: $9,000,000

- Investment portfolio: $5,500,000

- Real estate (multiple properties): $3,200,000

- Life insurance: $500,000

- Other assets: $300,000

Deductions:

- Funeral and administration: $280,000

- Debts and mortgages: $720,000

- Charitable bequest: $500,000

- Total deductions: $1,500,000

Adjusted Gross Estate = $18,500,000 − $1,500,000 = $17,000,000

Taxable Estate = $17,000,000 − $13,610,000 = $3,390,000

Applying the rate schedule:

$0–$1,000,000: Tax = $345,800 (from cumulative table)

$1,000,001–$3,390,000: $2,390,000 × 40% = $956,000

Total Estate Tax = $345,800 + $956,000 = $1,301,800

Approximation check: $3,390,000 × 40% = $1,356,000 (the approximation overstates slightly because rates below 40% apply to the first $1,000,000 of taxable estate)

Federal Estate Tax Owed: $1,301,800

Richard’s estate owes $1.3 million in federal estate tax — but retains $15.7 million in after-tax value for his heirs.

Example 3: Married Couple — Using Portability

Scenario: James and Carol, married. James dies in 2024. Estate planning uses portability to preserve both exemptions.

James’s estate at death: $8,000,000

- All assets left to Carol (surviving spouse)

- Unlimited marital deduction applies

Adjusted Gross Estate = $8,000,000

Marital Deduction = $8,000,000

Taxable Estate = $0

Federal Estate Tax on James's Death = $0

Portability election: Carol’s executor files IRS Form 706 within 9 months (or 15 months with extension) of James’s death to elect portability — preserving James’s unused exemption of $13,610,000 for Carol’s future estate.

Carol’s estate at her later death (assume estate has grown to $22,000,000):

Carol's Own Exemption: $13,610,000

James's Ported Exemption: $13,610,000 (preserved via portability election)

Total Available Exemption: $27,220,000

Taxable Estate = $22,000,000 − $27,220,000 = −$5,220,000

Federal Estate Tax = $0

By using portability, the couple transfers $22,000,000 to their heirs with zero federal estate tax — a result that would have been impossible without the timely portability election, and which illustrates why estate planning paperwork filed promptly after the first spouse’s death can be worth millions.

Example 4: The 2026 Exemption Sunset — Planning Urgency

Individual: Patricia, single, estate value $12,000,000

Under 2024 rules ($13.61M exemption):

Taxable Estate = $12,000,000 − $13,610,000 = −$1,610,000

Federal Estate Tax = $0

Under 2026 sunset rules (~$7M exemption, inflation-adjusted):

Taxable Estate = $12,000,000 − $7,000,000 = $5,000,000

Approximate Tax = $345,800 + ($4,000,000 × 40%) = $345,800 + $1,600,000 = $1,945,800

Federal Estate Tax ≈ $1,945,800

If Congress does not extend the current exemption, Patricia’s estate goes from owing zero to owing nearly $2 million — with no change in her actual wealth, only a change in the tax law. This is why estate attorneys and financial planners are urging clients with estates in the $7–$14 million range to act before the end of 2025.

State Estate Taxes

Twelve states and the District of Columbia impose their own estate taxes, entirely separate from the federal estate tax. Many have much lower exemption thresholds than the federal level, meaning estates that owe zero federal tax may still owe significant state estate tax.

States with Estate Taxes and Their 2024 Exemptions

| State | Exemption | Top Rate |

|---|---|---|

| Connecticut | $13,610,000 (matches federal) | 12% |

| Hawaii | $5,490,000 | 20% |

| Illinois | $4,000,000 | 16% |

| Maine | $6,410,000 | 12% |

| Maryland | $5,000,000 | 16% |

| Massachusetts | $2,000,000 | 16% |

| Minnesota | $3,000,000 | 16% |

| New York | $6,940,000 | 16% |

| Oregon | $1,000,000 | 16% |

| Rhode Island | $1,733,264 | 16% |

| Vermont | $5,000,000 | 16% |

| Washington State | $2,193,000 | 20% |

| Washington, D.C. | $4,528,800 | 16% |

State Estate Tax Example: Oregon

Oregon’s $1,000,000 exemption makes it one of the most aggressive state estate tax regimes in the country. An Oregon resident with an estate of $2,500,000 — well below the federal exemption and owing zero federal estate tax — would still owe Oregon state estate tax:

Oregon Taxable Estate = $2,500,000 − $1,000,000 = $1,500,000

Oregon Estate Tax (at blended rate ~10–14%): approximately $120,000–$210,000

Oregon residents with estates above $1,000,000 need state-level estate planning regardless of their federal tax position.

The “Cliff” in New York State Estate Tax

New York has an unusual “cliff” provision: if the estate exceeds the exemption by more than 5%, the entire estate — not just the excess — becomes subject to New York estate tax. This creates a situation where a $7,300,000 estate (just over the 5% cliff above the $6,940,000 exemption) may owe significantly more in New York estate tax than an estate of exactly $6,940,000.

The New York cliff is one of the most important — and counterintuitive — features in state estate tax law, and a compelling reason why New York residents near the exemption threshold benefit from careful planning.

The Gift Tax and Unified Lifetime Exemption

The estate tax does not exist in isolation — it is unified with the federal gift tax, which taxes large transfers made during life. The same $13.61 million lifetime exemption covers both gifts made during life and transfers at death.

How Lifetime Gifts Reduce the Estate Tax Exemption

Every taxable gift (gifts above the annual exclusion) made during life reduces the remaining exemption available at death:

Remaining Exemption at Death = $13,610,000 − Total Taxable Lifetime Gifts

Annual Gift Tax Exclusion: In 2024, each individual can give up to $18,000 per recipient per year without using any lifetime exemption. A married couple can give $36,000 per recipient per year using gift-splitting.

Strategic annual giving: A couple with three adult children and six grandchildren can give:

$36,000 × 9 recipients = $324,000 per year

…without touching the lifetime exemption and without any gift tax. Over 10 years, that removes $3,240,000 from the taxable estate — a meaningful reduction for large estates.

The 2026 Sunset and the “Anti-Clawback” Rule

A critical planning point for 2024 and 2025: the IRS has issued regulations clarifying that gifts made under the higher 2024 exemption will not be “clawed back” into the taxable estate if the exemption decreases in 2026. This means wealthy individuals can make large gifts now, locking in the higher exemption even if Congress reduces it later.

This anti-clawback protection is the primary driver of accelerated gifting strategies being implemented by high-net-worth individuals and their advisors in 2024 and 2025.

Legal Strategies to Reduce Estate Tax

For estates above or approaching the exemption threshold, numerous legal strategies can reduce or eliminate estate tax liability. These are not tax avoidance schemes — they are explicitly contemplated by the tax code.

Irrevocable Life Insurance Trust (ILIT)

Life insurance proceeds are included in the gross estate if the decedent owned the policy. Transferring ownership of a life insurance policy to an Irrevocable Life Insurance Trust (ILIT) removes the proceeds from the taxable estate. The ILIT owns the policy, pays premiums (funded by annual exclusion gifts), and receives the death benefit outside the estate — providing heirs with liquidity to pay estate taxes without the proceeds themselves being taxed.

Spousal Lifetime Access Trust (SLAT)

A SLAT allows one spouse to make an irrevocable gift to a trust for the benefit of the other spouse (and children), removing assets from the taxable estate while maintaining indirect access through the beneficiary spouse. SLATs are particularly popular in 2024–2025 as a strategy to lock in the high exemption before the sunset.

Grantor Retained Annuity Trust (GRAT)

A GRAT allows an individual to transfer assets expected to appreciate significantly into an irrevocable trust, receive annuity payments back for a fixed term, and pass any appreciation above the IRS’s assumed rate of return (the Section 7520 rate) to heirs free of gift and estate tax. GRATs work best in low-interest-rate environments, but any asset appreciation above the 7520 rate passes to beneficiaries estate-tax-free.

Charitable Remainder Trust (CRT)

A CRT transfers assets to a trust that pays income to the donor (or other named beneficiaries) for life or a fixed term, with the remainder passing to a charity at the end. The donor receives an immediate charitable deduction, removes assets from the taxable estate, and typically avoids capital gains tax on the sale of appreciated assets within the trust.

Qualified Personal Residence Trust (QPRT)

A QPRT allows a homeowner to transfer a primary or vacation residence to an irrevocable trust at a discounted gift tax value, retaining the right to live in the home for a fixed term. After the term, the home passes to heirs at a fraction of its full value for gift tax purposes. If the grantor survives the trust term, significant estate and gift tax savings result.

Family Limited Partnership (FLP)

A Family Limited Partnership consolidates family business or investment assets, allowing minority interest discounts of 20–40% to be applied when valuing interests transferred to heirs. A $1,000,000 FLP interest with a 30% minority discount is valued at $700,000 for estate and gift tax purposes — reducing taxable transfers while keeping assets consolidated under family control.

The Difference Between Estate Tax and Inheritance Tax

Estate tax is levied on the estate of the deceased before assets are distributed to heirs. It is paid by the estate itself, using estate assets.

Inheritance tax is levied on the recipients of an inheritance. The tax is paid by the beneficiaries, not the estate.

The United States has no federal inheritance tax. However, six states impose state inheritance taxes:

| State | Exemptions and Rates |

|---|---|

| Iowa | Phasing out; 0% for immediate family; up to 6% for others |

| Kentucky | Exempt for immediate family; 4–16% for others |

| Maryland | 0% for direct descendants; 10% for others (also has estate tax) |

| Nebraska | Exempt for immediate family up to $100,000; 1–18% for others |

| New Jersey | Exempt for direct descendants; 11–16% for others |

| Pennsylvania | 0% for spouses; 4.5% for children; 12% for siblings; 15% for others |

Maryland is the only state with both an estate tax and an inheritance tax — a dual burden for estates in that state.

Estate Tax vs. Income Tax on Inherited Assets

Estate tax and income tax are separate systems that can both apply to inherited wealth, but they generally apply to different things:

Estate tax applies to the value of assets at the time of death — the transfer itself.

Income tax applies when inherited assets generate income after transfer. Inherited traditional IRA and 401(k) accounts are subject to income tax when distributions are taken (inherited IRAs now require full distribution within 10 years under the SECURE Act 2.0 for most non-spouse beneficiaries).

The step-up in basis: Inherited non-retirement assets (stocks, real estate, business interests) generally receive a step-up in cost basis to the fair market value at the date of death. An heir who inherits stock purchased for $50,000 that is worth $500,000 at death owes no capital gains tax on that $450,000 of appreciation — it is effectively forgiven through the step-up. This is one of the most valuable tax benefits in the estate system and a powerful incentive for holding appreciated assets until death rather than selling during life.

Frequently Asked Questions

What is the estate tax exemption for 2024?

The federal estate tax exemption for 2024 is $13,610,000 per individual, or $27,220,000 for a married couple using portability. Estates below these thresholds owe no federal estate tax.

What is the federal estate tax rate?

The federal estate tax is progressive, with rates ranging from 18% to 40% on the taxable estate (the amount above the exemption). In practice, because the exemption absorbs all income up to $13.61 million, virtually any taxable amount above the exemption is subject to the 40% top rate.

Do most people owe estate tax?

No. Fewer than 0.1% of estates owe federal estate tax due to the high exemption threshold. However, 12 states and D.C. impose their own estate taxes with much lower exemptions — Oregon’s $1,000,000 threshold, for example, captures many middle-class estates.

What happens to the estate tax exemption in 2026?

Unless Congress acts to extend the current provisions, the Tax Cuts and Jobs Act (TCJA) estate tax changes are scheduled to sunset on January 1, 2026, reducing the exemption to approximately $7 million per individual (inflation-adjusted). This is the most urgent estate planning consideration for individuals with estates in the $7–$14 million range.

What is portability in estate tax?

Portability allows a surviving spouse to use the deceased spouse’s unused estate tax exemption by filing IRS Form 706 within 9 months (or 15 months with extension) of death. This effectively doubles the estate tax exemption for married couples to $27.22 million in 2024.

What is the difference between estate tax and inheritance tax?

Estate tax is paid by the estate before assets are distributed to heirs. Inheritance tax is paid by the heirs after they receive assets. The U.S. has no federal inheritance tax, but six states (Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania) impose state inheritance taxes.

What is the step-up in basis for inherited assets?

Inherited non-retirement assets receive a step-up in cost basis to the fair market value at the date of death, eliminating capital gains tax on all appreciation that occurred during the decedent’s lifetime. This is one of the most valuable tax benefits associated with inherited wealth.

How can I reduce my estate tax liability?

Legal strategies include maximizing annual exclusion gifts ($18,000 per recipient in 2024), establishing irrevocable trusts (ILIT, SLAT, GRAT, CRT, QPRT), using family limited partnerships with minority interest discounts, making charitable bequests, and — for 2024 and 2025 specifically — making large gifts to lock in the higher exemption before a potential 2026 sunset.

Conclusion

An estate tax calculator transforms one of the most complex areas of tax law into a concrete, quantifiable number — the amount of wealth that will transfer to heirs versus the amount that will be paid in taxes at death. For the vast majority of Americans, that number is zero: the federal exemption is high enough that estate tax is not a factor. For estates in the $7–$27 million range, however, the 2026 sunset makes the next 12–18 months one of the most consequential planning windows in a generation.

The formula itself is methodical: gross estate minus deductions minus exemption, multiplied by the applicable rate. The complexity lives in the details — which assets are included, which deductions apply, how state taxes layer on top, how portability works, and which planning strategies reduce the taxable estate before the calculation is ever made.

Estate planning is ultimately an act of intention — deciding deliberately how accumulated wealth will transfer to the next generation, rather than leaving that decision to the default rules of the tax code. The estate tax calculator is the tool that makes that intention concrete.

Related Topics

- Sales Tax Calculator: Formula, Examples, and How It Works

- Income Tax Basics Explained: Brackets, Deductions, and Real-World Examples

- Marriage Tax Calculator: Formula, Examples, and How It Works

- Time and a Half Calculator: Formula, Examples, and How It Works

- Rent Calculator: Formula, Examples, and How It Works