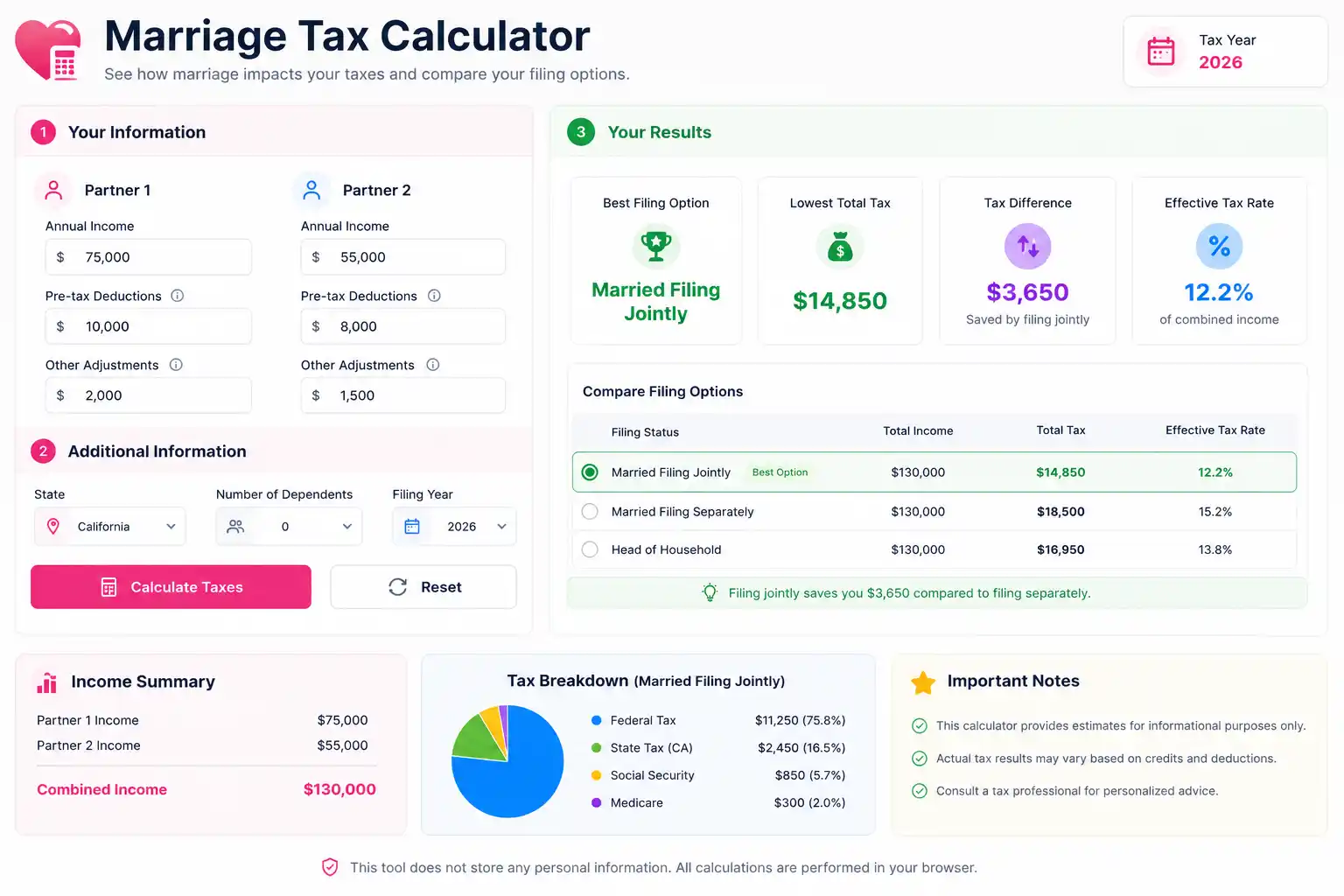

What Is a Marriage Tax Calculator?

A marriage tax calculator is a financial tool that compares the combined federal income tax liability of two people filing as single versus filing jointly (or separately) as a married couple — revealing whether marriage produces a tax penalty (the couple pays more taxes married than they would as singles) or a tax bonus (they pay less).

The result is not random. It is a predictable mathematical consequence of how the U.S. federal income tax system structures its brackets, standard deductions, phase-outs, and credits for different filing statuses. Whether a couple faces a penalty or a bonus depends primarily on one variable: how similar or different their individual incomes are.

For millions of American couples, marriage has a meaningful tax consequence — either direction — that can amount to hundreds or thousands of dollars per year. A marriage tax calculator makes that consequence visible and quantifiable before or after the wedding, giving couples the financial information they need to make informed decisions about filing status, withholding, retirement contributions, and tax planning.

The Marriage Penalty vs. Marriage Bonus: The Core Concept

The Marriage Penalty

A marriage penalty exists when a married couple filing jointly pays more in combined federal income tax than they would have paid as two single filers. It occurs most commonly when both spouses earn similar incomes — particularly when both are in the same or adjacent tax brackets.

The structural cause: the income thresholds for upper tax brackets in the Married Filing Jointly (MFJ) status are less than double the thresholds for Single filers. When two similar-earning singles combine their income, a portion of that combined income gets pushed into a higher bracket that neither would have reached alone.

The Marriage Bonus

A marriage bonus exists when a married couple filing jointly pays less in combined federal income tax than they would have paid as two single filers. It occurs most commonly when there is a significant income disparity between spouses — one earner is significantly higher than the other, or one spouse has little or no income.

The structural cause: the lower-earning spouse’s income gets effectively taxed at the marginal rates that begin at zero — using the space at the bottom of the joint bracket schedule rather than being “stacked” on top of the higher earner’s income. The result is a lower blended effective rate than either spouse would have achieved filing alone.

The Fundamental Rule

If Spouse A Income ≈ Spouse B Income → Likely Marriage Penalty

If Spouse A Income >> Spouse B Income → Likely Marriage Bonus

If one spouse has zero income → Guaranteed Marriage Bonus

2024 Federal Tax Brackets: Single vs. Married Filing Jointly

The marriage penalty and bonus are embedded directly in the tax bracket structure. Comparing the two schedules reveals exactly where the disparity occurs.

2024 Federal Tax Brackets — Single Filers

| Tax Rate | Income Range |

|---|---|

| 10% | $0 – $11,600 |

| 12% | $11,601 – $47,150 |

| 22% | $47,151 – $100,525 |

| 24% | $100,526 – $191,950 |

| 32% | $191,951 – $243,725 |

| 35% | $243,726 – $609,350 |

| 37% | Over $609,350 |

2024 Federal Tax Brackets — Married Filing Jointly

| Tax Rate | Income Range |

|---|---|

| 10% | $0 – $23,200 |

| 12% | $23,201 – $94,300 |

| 22% | $94,301 – $201,050 |

| 24% | $201,051 – $383,900 |

| 32% | $383,901 – $487,450 |

| 35% | $487,451 – $731,200 |

| 37% | Over $731,200 |

Where the Penalty Is Embedded

For tax rates through 24%, the MFJ bracket thresholds are exactly double the Single thresholds. At those levels there is bracket neutrality — no marriage penalty or bonus from brackets alone.

The penalty emerges at the 32% bracket and above:

| Rate | Single Threshold | MFJ Threshold | MFJ vs. 2× Single |

|---|---|---|---|

| 32% | $191,951 | $383,901 | Exactly 2× — neutral |

| 35% | $243,726 | $487,451 | $487,451 vs. $487,452 — nearly neutral |

| 37% | $609,350 | $731,200 | $731,200 vs. $1,218,700 — significant penalty |

The most severe bracket-driven marriage penalty occurs at the top: two singles each earning $609,350 ($1,218,700 combined) would each be in the 37% bracket on income above their individual thresholds. As a married couple, the 37% bracket begins at $731,200 — meaning $487,500 of their combined income that would have been taxed at 37% as singles is now taxed at 35%, creating a bonus at this extreme. However, for high earners in the $300,000–$700,000 combined income range, the penalty is more common.

The Standard Deduction

The 2024 standard deduction also shapes the marriage tax outcome:

| Filing Status | 2024 Standard Deduction |

|---|---|

| Single | $14,600 |

| Married Filing Jointly | $29,200 |

| Married Filing Separately | $14,600 |

The MFJ standard deduction is exactly double the Single deduction — perfectly neutral. No marriage penalty or bonus comes from the standard deduction alone.

The Marriage Tax Calculator Formula

The calculation compares tax liability under two scenarios and finds the difference:

Step 1: Calculate Each Person’s Tax as Single

For each spouse individually, calculate federal income tax using single filing status and the single standard deduction:

Single Tax (Spouse A) = Tax on (Gross Income A − $14,600) using Single brackets

Single Tax (Spouse B) = Tax on (Gross Income B − $14,600) using Single brackets

Combined Single Tax = Single Tax A + Single Tax B

Step 2: Calculate the Couple’s Tax as Married Filing Jointly

Combine incomes and calculate tax using MFJ brackets and MFJ standard deduction:

Joint Taxable Income = (Gross Income A + Gross Income B) − $29,200

Joint Tax = Tax on Joint Taxable Income using MFJ brackets

Step 3: Calculate the Marriage Penalty or Bonus

Marriage Penalty/Bonus = Joint Tax − Combined Single Tax

Positive result = Marriage Penalty (pay more when married)

Negative result = Marriage Bonus (pay less when married)

Step-by-Step Marriage Tax Calculation Examples

Example 1: Similar Incomes — Marriage Penalty

Couple: David and Mia David’s Income: $85,000 Mia’s Income: $80,000 Combined Income: $165,000

As Single Filers:

David’s taxable income: $85,000 − $14,600 = $70,400

10% on $11,600 = $1,160

12% on $35,550 ($11,601–$47,150) = $4,266

22% on $23,250 ($47,151–$70,400) = $5,115

David's Single Tax = $10,541

Mia’s taxable income: $80,000 − $14,600 = $65,400

10% on $11,600 = $1,160

12% on $35,550 = $4,266

22% on $18,250 ($47,151–$65,400) = $4,015

Mia's Single Tax = $9,441

Combined Single Tax: $10,541 + $9,441 = $19,982

As Married Filing Jointly:

Joint taxable income: $165,000 − $29,200 = $135,800

10% on $23,200 = $2,320

12% on $71,100 ($23,201–$94,300) = $8,532

22% on $41,500 ($94,301–$135,800) = $9,130

Joint Tax = $19,982

Marriage Penalty/Bonus: $19,982 − $19,982 = $0

At these income levels (both under the 22%/24% bracket boundary), David and Mia face neither a penalty nor a bonus — the brackets are perfectly doubled in the 22% range, producing exact neutrality. The penalty starts to bite as combined income crosses the 24% and higher brackets.

Example 2: Similar High Incomes — Clear Marriage Penalty

Couple: Jordan and Alex Jordan’s Income: $200,000 Alex’s Income: $180,000 Combined Income: $380,000

As Single Filers:

Jordan’s taxable income: $200,000 − $14,600 = $185,400

10% on $11,600 = $1,160

12% on $35,550 = $4,266

22% on $53,375 ($47,151–$100,525) = $11,743

24% on $85,400 ($100,526–$185,400) [capped at $185,400] = $20,496

Jordan's Single Tax = $37,665

Alex’s taxable income: $180,000 − $14,600 = $165,400

10% on $11,600 = $1,160

12% on $35,550 = $4,266

22% on $53,375 = $11,743

24% on $64,875 ($100,526–$165,400) = $15,570

Alex's Single Tax = $32,739

Combined Single Tax: $37,665 + $32,739 = $70,404

As Married Filing Jointly:

Joint taxable income: $380,000 − $29,200 = $350,800

10% on $23,200 = $2,320

12% on $71,100 = $8,532

22% on $106,750 ($94,301–$201,050) = $23,485

24% on $149,750 ($201,051–$350,800) = $35,940

Joint Tax = $70,277

Marriage Penalty/Bonus: $70,277 − $70,404 = −$127

Interestingly, at this combined income level the couple still has a very slight bonus of $127 — the bracket doubling is nearly perfect through the 24% range. The penalty becomes more pronounced as income pushes into the 32%, 35%, and especially the 37% brackets.

Example 3: Disparate Incomes — Marriage Bonus

Couple: Chris and Taylor Chris’s Income: $120,000 Taylor’s Income: $28,000 Combined Income: $148,000

As Single Filers:

Chris’s taxable income: $120,000 − $14,600 = $105,400

10% on $11,600 = $1,160

12% on $35,550 = $4,266

22% on $53,375 = $11,743

24% on $4,875 ($100,526–$105,400) = $1,170

Chris's Single Tax = $18,339

Taylor’s taxable income: $28,000 − $14,600 = $13,400

10% on $11,600 = $1,160

12% on $1,800 ($11,601–$13,400) = $216

Taylor's Single Tax = $1,376

Combined Single Tax: $18,339 + $1,376 = $19,715

As Married Filing Jointly:

Joint taxable income: $148,000 − $29,200 = $118,800

10% on $23,200 = $2,320

12% on $71,100 = $8,532

22% on $24,500 ($94,301–$118,800) = $5,390

Joint Tax = $16,242

Marriage Penalty/Bonus: $16,242 − $19,715 = −$3,473

Marriage Bonus: $3,473 — Chris and Taylor save $3,473 per year by filing jointly as a married couple versus filing as singles.

Example 4: One Non-Working Spouse — Maximum Marriage Bonus

Couple: Morgan (earns $95,000) and Sam (no income)

As Single Filers:

Morgan’s taxable income: $95,000 − $14,600 = $80,400

10% on $11,600 = $1,160

12% on $35,550 = $4,266

22% on $33,250 ($47,151–$80,400) = $7,315

Morgan's Single Tax = $12,741

Sam's Single Tax = $0

Combined Single Tax: $12,741

As Married Filing Jointly:

Joint taxable income: $95,000 − $29,200 = $65,800

10% on $23,200 = $2,320

12% on $42,600 ($23,201–$65,800) = $5,112

Joint Tax = $7,432

Marriage Penalty/Bonus: $7,432 − $12,741 = −$5,309

Marriage Bonus: $5,309 — the single-income household saves over $5,300 per year through joint filing, as Sam’s zero income effectively gives Morgan access to a larger tax-free income range and lower marginal rates on the early portions of income.

Beyond Brackets: Other Marriage Tax Impacts

The bracket comparison above captures the most visible marriage tax effect, but several other provisions in the tax code also change significantly upon marriage — sometimes creating additional penalties, sometimes additional benefits.

Child Tax Credit Phase-Out

The Child Tax Credit ($2,000 per qualifying child in 2024) begins phasing out at:

- Single: $200,000 AGI

- MFJ: $400,000 AGI

The MFJ threshold is exactly double the single threshold — producing no marriage penalty for this credit.

SALT Deduction Cap

The $10,000 cap on the State and Local Tax (SALT) deduction applies equally to both single filers and married couples filing jointly — effectively a $10,000 cap per return regardless of status. This is one of the most explicit marriage penalties in the current tax code: two singles could each deduct up to $10,000 ($20,000 combined), while the same two people married can only deduct $10,000 total — a $10,000 reduction in potential deductions.

For high-tax states (California, New York, New Jersey, Massachusetts), the SALT cap marriage penalty can add $2,200–$3,700 to a couple’s annual federal tax bill, depending on their marginal rate.

Net Investment Income Tax (NIIT)

The 3.8% NIIT applies to investment income above:

- Single: $200,000 AGI

- MFJ: $250,000 AGI (not $400,000 — not doubled)

This is a clear marriage penalty at high income levels. Two singles each earning $220,000 in investment income ($440,000 combined) would not individually trigger NIIT. As a married couple with $440,000 AGI, $190,000 of their investment income is subject to the 3.8% NIIT — a $7,220 penalty per year from this provision alone.

Student Loan Income-Driven Repayment

For borrowers on income-driven repayment (IDR) plans, marriage affects monthly payment calculations because spousal income may be included in Adjusted Gross Income. Married borrowers filing jointly often face significantly higher monthly payments. Some couples strategically file Married Filing Separately to exclude spousal income from IDR calculations — accepting a higher tax bill in exchange for lower student loan payments.

Social Security Benefits

Married couples may receive certain Social Security spousal and survivor benefits unavailable to single individuals — a financial advantage of marriage that exists outside the income tax calculation but contributes to the overall financial picture.

Capital Gains Tax Brackets

Long-term capital gains rates have their own bracket structure, and the 0% rate threshold:

- Single: $47,025

- MFJ: $94,050 (exactly doubled — no penalty here)

Married Filing Separately: When It Makes Sense

Married Filing Separately (MFS) is the often-overlooked third option for married couples. It taxes each spouse on their own income using separate brackets that are identical to Single brackets in most cases — but with some significant disadvantages:

MFS disadvantages:

- Standard deduction: $14,600 (half of MFJ)

- Cannot claim the Earned Income Tax Credit

- Cannot claim the Child and Dependent Care Credit

- Cannot deduct student loan interest

- Roth IRA contribution phase-out begins at $0 AGI (vs. $230,000 for MFJ in 2024)

- Social Security benefits become more taxable at lower thresholds

MFS may be beneficial when:

- One spouse has significant medical expenses (deductible above 7.5% of AGI; keeping AGI separate preserves the deduction)

- One spouse is on income-driven student loan repayment

- One spouse has significant miscellaneous itemized deductions

- Spouses are legally separated and choose not to commingle tax liability

- One spouse suspects the other of tax fraud (innocent spouse protection)

The decision to file MFS should always involve a tax professional comparing the total liability across all three options: Single (if divorcing), MFJ, and MFS.

Strategies to Minimize the Marriage Tax Penalty

For couples who discover they face a marriage penalty, several legal strategies can reduce the impact:

Maximize Retirement Contributions

Pre-tax contributions to 401(k), 403(b), and traditional IRA accounts reduce AGI — potentially shifting income out of higher brackets. For a couple both contributing the maximum 401(k) ($23,000 each in 2024), combined AGI is reduced by $46,000, which can meaningfully reduce or eliminate a bracket-driven penalty.

Manage Investment Income Timing

For couples near the NIIT threshold or capital gains bracket boundaries, timing the realization of investment gains across tax years — harvesting gains in lower-income years and deferring in higher-income years — can minimize the NIIT marriage penalty.

HSA Contributions

Health Savings Account contributions reduce AGI dollar-for-dollar. A family HSA contribution ($8,300 in 2024) reduces combined AGI by $8,300, potentially moving the couple into a lower bracket or below a phase-out threshold.

Consider Business Structure

Self-employed spouses can sometimes shift income between business entities in ways that balance adjusted gross incomes more evenly — reducing bracket disparity — or deduct business expenses that effectively reduce taxable income before the marriage penalty calculation applies.

Qualified Business Income (QBI) Deduction

Pass-through business owners may deduct up to 20% of qualified business income under Section 199A. The phase-out range for this deduction is higher for MFJ filers than for singles, which can be a meaningful marriage bonus for couples with pass-through business income.

Frequently Asked Questions

What is the marriage tax penalty?

The marriage tax penalty occurs when a married couple filing jointly pays more in combined federal income tax than they would have paid as two single filers. It most commonly affects couples with similar incomes, particularly at higher income levels where tax bracket thresholds are less than double the single thresholds.

Do all married couples pay more taxes?

No. Couples with significant income disparity — especially single-income households — often pay less as a married couple than they would as singles. This is called the marriage bonus. The outcome depends primarily on how similar the two spouses’ incomes are.

How do I calculate the marriage tax penalty or bonus?

Calculate each spouse’s federal income tax as if they were still single. Add those two amounts together. Then calculate the couple’s tax filing jointly. The difference (joint tax minus combined single tax) is the marriage penalty (if positive) or marriage bonus (if negative).

What income level has the worst marriage penalty?

The marriage penalty is most severe for high-income couples where both spouses have similar incomes in the 35%–37% bracket range. The SALT deduction cap also creates an additional penalty for high earners in high-tax states regardless of income level.

Can married couples file taxes separately?

Yes. Married Filing Separately (MFS) is a legal filing status, but it comes with significant disadvantages — the loss of numerous credits and deductions. It is typically only beneficial in specific situations involving income-driven student loan repayment, large medical deductions, or liability separation concerns.

Does marriage affect the standard deduction?

The Married Filing Jointly standard deduction ($29,200 in 2024) is exactly double the Single standard deduction ($14,600). There is no marriage penalty or bonus from the standard deduction alone.

How does the SALT cap create a marriage penalty?

The $10,000 SALT deduction cap applies per tax return, not per person. Two singles can each deduct up to $10,000 ($20,000 combined), while a married couple filing jointly can only deduct $10,000 total — a direct $10,000 reduction in deductible state and local taxes that creates a measurable marriage penalty for itemizers in high-tax states.

Should I adjust my withholding after getting married?

Yes. Marriage changes your filing status and potentially your tax bracket, which can affect whether you are over- or under-withholding throughout the year. File a new W-4 with your employer after marriage, using the IRS Tax Withholding Estimator to calculate the correct withholding for your new combined income situation.

Conclusion

A marriage tax calculator reveals what the wedding invitation never mentions: the federal income tax code has a measurable opinion about how similar your incomes are. Couples with similar earnings — particularly at higher income levels — frequently pay a marriage penalty, while couples with disparate incomes enjoy a bonus. The difference can range from negligible to several thousand dollars per year, depending on the income combination.

Understanding your marriage tax outcome is not about making decisions based on tax consequences alone — it is about entering married financial life with complete information. Whether you discover a penalty or a bonus, that knowledge informs retirement contribution decisions, withholding adjustments, filing status strategy, and the conversations you have with a tax professional about optimizing your combined tax position.

The tax code did not design its marriage provisions to be punitive or rewarding — they are the emergent result of a system that was designed separately and imperfectly merged. The couples who navigate it best are the ones who understand exactly what those merged rules mean for their specific numbers.

Related Topics

- Income Tax Basics Explained: Brackets, Deductions, and Real-World Examples

- Sales Tax Calculator: Formula, Examples, and How It Works

- Time and a Half Calculator: Formula, Examples, and How It Works

- Rent Calculator: Formula, Examples, and How It Works

- House Affordability Calculator: Formula, Examples, and How It Works