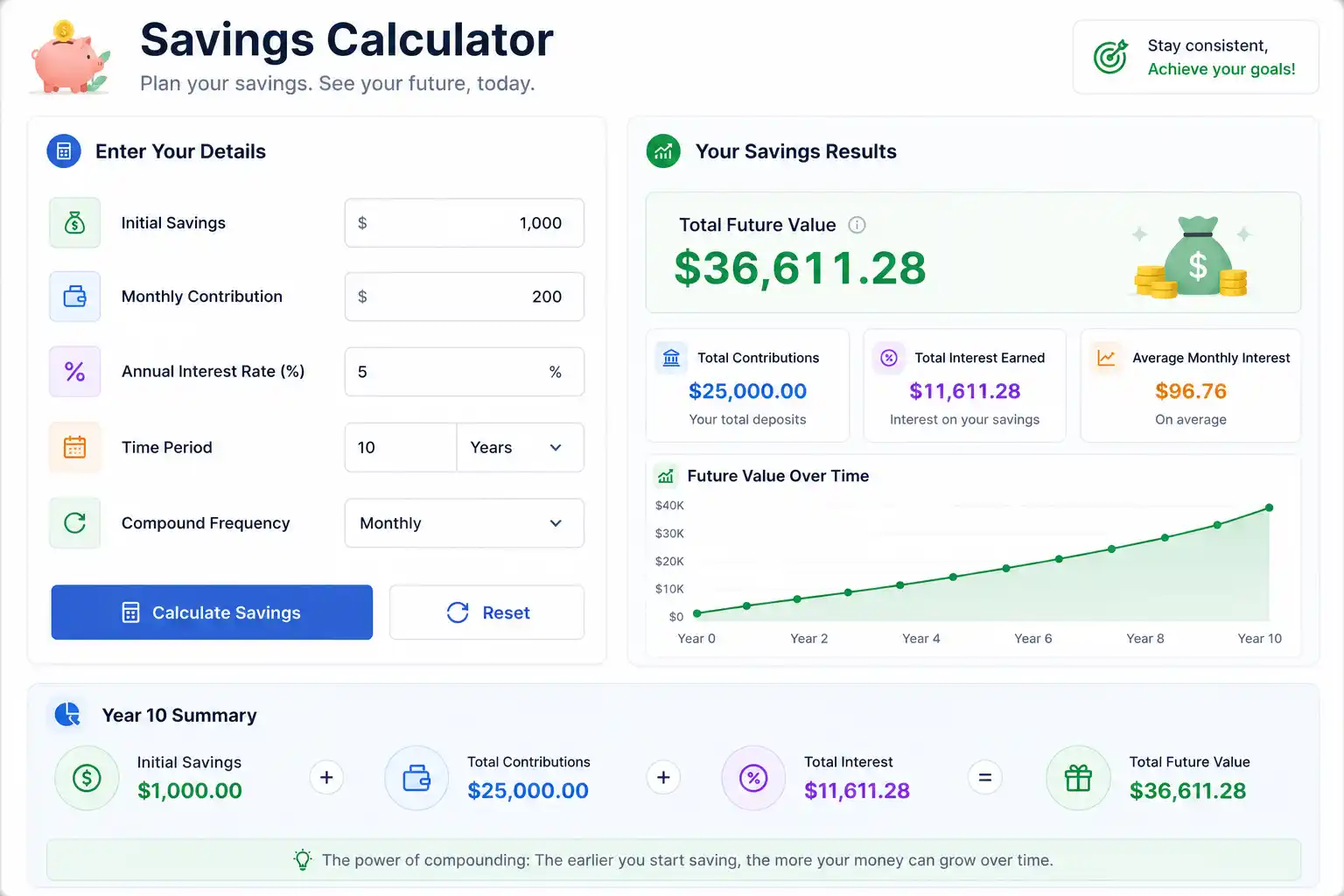

What Is a Savings Calculator?

A savings calculator is a financial planning tool that projects how much money you will accumulate over a defined period based on your initial deposit, regular contributions, interest rate, and compounding frequency. It answers the questions that matter most to savers: How much will I have in 10 years? How much do I need to save each month to reach my goal? How much does the interest rate actually matter?

The tool is deceptively simple to use and mathematically profound in its implications. Feed in a few numbers — starting balance, monthly contribution, annual interest rate, time horizon — and the calculator returns a future value that most people find either surprisingly encouraging or sobering, depending on whether they started saving early or late.

Savings calculators are used for goals across the financial spectrum: building an emergency fund, saving for a down payment, funding a child’s education, planning a vacation, or simply understanding how a savings account, CD, money market account, or high-yield savings account will grow over time. The formula underneath every one of these use cases is the same — compound interest — and understanding it changes how intelligently you use every savings tool available to you.

The Mathematics of Saving: Simple vs. Compound Interest

Before diving into the full savings calculator formula, understanding the distinction between simple and compound interest is essential. The difference between the two is not academic — it is the difference between linear and exponential growth, and over time, the gap becomes enormous.

Simple Interest

Simple interest calculates returns only on the original principal. It does not earn interest on previously earned interest.

Simple Interest = Principal × Rate × Time

Future Value = Principal + Simple Interest

Example: $10,000 at 5% simple interest for 10 years:

Simple Interest = $10,000 × 0.05 × 10 = $5,000

Future Value = $10,000 + $5,000 = $15,000

Simple interest is used for some short-term loans and bonds but is rarely applied to savings accounts. Almost all savings products use compound interest.

Compound Interest

Compound interest calculates returns on both the original principal AND the interest already earned. Each compounding period, the interest is added to the balance, and the next period’s interest is calculated on this larger amount. This is the mechanism behind exponential growth — what Albert Einstein reportedly called the eighth wonder of the world.

Future Value = Principal × (1 + Rate/n)^(n×t)

Where:

- Principal = starting balance

- Rate = annual interest rate (as a decimal)

- n = number of compounding periods per year

- t = time in years

Same example with compound interest: $10,000 at 5% compounded monthly for 10 years:

FV = $10,000 × (1 + 0.05/12)^(12×10)

= $10,000 × (1.004167)^120

= $10,000 × 1.6471

= $16,470.09

The difference: $1,470.09 more from compounding alone, with no additional deposits. Over longer periods and with higher balances, this gap becomes thousands or tens of thousands of dollars.

The Complete Savings Calculator Formula

Most savings calculators go beyond simple lump-sum deposits — they account for regular contributions made over time (monthly deposits into a savings account, for example). The formula that handles both is the future value of a series with an initial lump sum:

FV = P × (1 + r/n)^(n×t) + PMT × [((1 + r/n)^(n×t) − 1) / (r/n)]

Where:

- FV = Future Value (the amount you’ll have at the end)

- P = Principal (initial deposit / starting balance)

- r = Annual interest rate (as a decimal; 5% = 0.05)

- n = Compounding periods per year (monthly = 12, quarterly = 4, daily = 365)

- t = Time in years

- PMT = Regular periodic payment/contribution amount

Breaking the Formula Into Two Parts

Part 1 — Growth of the initial deposit:

P × (1 + r/n)^(n×t)

Part 2 — Growth of regular contributions (future value of an annuity):

PMT × [((1 + r/n)^(n×t) − 1) / (r/n)]

Adding both parts gives the total future value.

Compounding Frequency: How Often Interest Is Calculated

The compounding frequency — how often interest is added to the account balance — materially affects the final value. The more frequently interest compounds, the faster the balance grows.

| Compounding Frequency | n (periods/year) | $10,000 at 5% for 10 years |

|---|---|---|

| Annually | 1 | $16,288.95 |

| Semi-annually | 2 | $16,386.16 |

| Quarterly | 4 | $16,436.19 |

| Monthly | 12 | $16,470.09 |

| Daily | 365 | $16,486.65 |

| Continuously | e^(r×t) | $16,487.21 |

The difference between annual and daily compounding on $10,000 over 10 years is $197.26 — meaningful, but less dramatic than most people expect. The compounding frequency matters far less than the interest rate and the time horizon.

Step-by-Step Savings Calculation Examples

Example 1: Emergency Fund Goal

Goal: Build a $15,000 emergency fund Starting Balance: $2,000 Monthly Contribution: $300 Annual Interest Rate: 4.5% (high-yield savings account) Compounding: Monthly (n = 12) Time: How long will it take?

Using the formula iteratively (or a calculator solving for t):

r/n = 0.045/12 = 0.00375

After 12 months:

FV = 2,000 × (1.00375)^12 + 300 × [((1.00375)^12 − 1) / 0.00375]

= 2,000 × 1.04594 + 300 × [0.04594 / 0.00375]

= $2,091.88 + 300 × 12.251

= $2,091.88 + $3,675.30

= $5,767.18 after 1 year

After 24 months (2 years):

FV ≈ $9,732.05

After 36 months (3 years):

FV ≈ $13,919.22

After 40 months (~3 years 4 months):

FV ≈ $15,068.14 ✓

Result: Reaching the $15,000 goal takes approximately 3 years and 4 months with $300/month and a 4.5% rate.

What if the rate were only 0.5% (traditional savings account)? At 0.5%, the same $300/month with a $2,000 start reaches $15,000 in approximately 3 years and 8 months — just 4 months longer. For shorter goals, the rate matters less than consistency of contributions.

Example 2: Down Payment Savings Goal

Goal: $60,000 down payment for a home Starting Balance: $10,000 Monthly Contribution: $800 Annual Interest Rate: 4.75% (high-yield savings) Compounding: Monthly Time: 5 years

r/n = 0.0475/12 = 0.003958

FV = 10,000 × (1.003958)^60 + 800 × [((1.003958)^60 − 1) / 0.003958]

(1.003958)^60 = 1.2694

Part 1: 10,000 × 1.2694 = $12,694.00

Part 2: 800 × [(1.2694 − 1) / 0.003958]

= 800 × [0.2694 / 0.003958]

= 800 × 68.06

= $54,448.00

FV = $12,694.00 + $54,448.00 = $67,142.00

Result: After 5 years, the projected balance is $67,142 — exceeding the $60,000 goal by $7,142. The buyer could reduce their monthly contribution to approximately $710/month and still reach the goal.

Example 3: Long-Term Wealth Building

Scenario: A 25-year-old saving for retirement at 65 (40-year horizon) Starting Balance: $5,000 Monthly Contribution: $500 Annual Interest Rate: 7% (historical average stock market return, net of inflation is lower — used here to illustrate compounding only) Compounding: Monthly

r/n = 0.07/12 = 0.005833

(1.005833)^480 = 14.7306

Part 1: 5,000 × 14.7306 = $73,653.00

Part 2: 500 × [(14.7306 − 1) / 0.005833]

= 500 × [13.7306 / 0.005833]

= 500 × 2,353.6

= $1,176,800.00

FV = $73,653 + $1,176,800 = $1,250,453

Total contributions over 40 years: $5,000 + (500 × 480 months) = $245,000 Interest earned: $1,250,453 − $245,000 = $1,005,453

Over 40 years, interest and compounding generate more than four times the money contributed — the most powerful illustration of why starting early is the single most impactful savings decision anyone can make.

Example 4: The Cost of Waiting 10 Years

The most common personal finance comparison: what happens when two people start saving at different ages with otherwise identical parameters.

Person A starts at age 25:

- Monthly contribution: $400/month for 40 years (until age 65)

- Annual rate: 6%

- Total contributions: $192,000

- Estimated Future Value: ~$800,000

Person B starts at age 35:

- Monthly contribution: $400/month for 30 years (until age 65)

- Annual rate: 6%

- Total contributions: $144,000

- Estimated Future Value: ~$402,000

Person A ends up with nearly double the balance despite contributing only $48,000 more. The additional $398,000 came entirely from 10 extra years of compounding — the decade between age 25 and 35. This is the most concrete illustration of why financial advisors universally prioritize starting early over contributing more later.

How Interest Rates Affect Savings Growth

Interest rate differences that look small on paper produce enormous differences over time. Here is the future value of $10,000 with $300/month contributions at various rates over 20 years:

| Annual Rate | FV After 20 Years | Total Contributed | Interest Earned |

|---|---|---|---|

| 0.5% | $84,320 | $82,000 | $2,320 |

| 1.5% | $88,757 | $82,000 | $6,757 |

| 3.0% | $99,151 | $82,000 | $17,151 |

| 4.5% | $111,699 | $82,000 | $29,699 |

| 5.0% | $117,288 | $82,000 | $35,288 |

| 6.0% | $130,226 | $82,000 | $48,226 |

| 7.0% | $145,072 | $82,000 | $63,072 |

| 8.0% | $162,123 | $82,000 | $80,123 |

The difference between 0.5% (a traditional savings account rate in low-interest environments) and 5.0% (a high-yield savings account or short-term CD rate in a higher-rate environment) is $32,968 on the same contributions over 20 years. Chasing a better savings rate is not trivial — it has compounding consequences.

Types of Savings Accounts and Their Rates

The savings calculator formula applies identically regardless of the account type — what changes is the interest rate input and sometimes the compounding frequency.

High-Yield Savings Accounts (HYSA)

Online banks and credit unions frequently offer high-yield savings accounts with APYs significantly above the national average. As of mid-2026, competitive HYSAs offer rates in the 4.0–5.5% APY range (subject to change with Federal Reserve policy). Interest typically compounds daily and credits monthly.

Certificates of Deposit (CDs)

CDs lock in a fixed interest rate for a defined term — 3 months, 6 months, 1 year, 2 years, 5 years. They typically offer higher rates than savings accounts in exchange for reduced liquidity. Early withdrawal penalties apply if funds are accessed before the maturity date. CD rates use the same compounding formula with n matching the CD’s compounding frequency.

Money Market Accounts (MMAs)

Money market accounts combine features of savings and checking accounts, offering higher rates than traditional savings with limited check-writing ability. Rates are variable and typically competitive with high-yield savings accounts.

Treasury Bills and I-Bonds

U.S. government savings instruments. I-Bonds carry a fixed rate component plus an inflation adjustment component, making them particularly valuable as an inflation hedge. The savings calculator formula applies to the fixed rate component; the inflation component adds variable return.

529 Education Savings Plans

Tax-advantaged accounts for education expenses. Returns depend on the underlying investment options selected — from FDIC-insured savings options (using the standard savings calculator formula) to equity-based portfolios (requiring investment return projections rather than fixed rate calculations).

The APY vs. APR Distinction

Every savings calculator requires an interest rate input, and understanding whether you are inputting an APR (Annual Percentage Rate) or APY (Annual Percentage Yield) determines whether the formula needs additional conversion.

APR is the raw annual interest rate before compounding effects.

APY already accounts for compounding — it is the effective annual rate earned after compounding is applied within the year.

APY = (1 + APR/n)^n − 1

Example:

- APR: 5.00%

- Compounding: Monthly (n = 12)

- APY = (1 + 0.05/12)^12 − 1 = (1.004167)^12 − 1 = 0.05116 = 5.116%

When a bank advertises an APY, you can use it directly as the rate in the savings formula with annual compounding (n=1) and get the same result as using the APR with monthly compounding (n=12). Savings account advertisements almost always display APY — use that figure and set n=1, or convert back to APR for the full formula.

Rule of thumb: If the rate comes from a bank advertisement, it is almost certainly an APY. Use it with n=1 in the formula, or use the dedicated APY input option in any online savings calculator.

How to Calculate Savings Goals: Working Backward

Sometimes the question is not “how much will I have?” but “how much do I need to save each month to reach my goal?” The savings calculator formula can be rearranged to solve for the required monthly payment (PMT):

PMT = (FV − P × (1 + r/n)^(n×t)) × (r/n) / ((1 + r/n)^(n×t) − 1)

Required Monthly Savings Examples

Goal: $25,000 vacation fund in 3 years Starting Balance: $3,000 Annual Rate: 4.5% (monthly compounding)

r/n = 0.00375

(1.00375)^36 = 1.14423

Part 1 growth: 3,000 × 1.14423 = $3,432.69

Remaining needed: $25,000 − $3,432.69 = $21,567.31

PMT = $21,567.31 × 0.00375 / (1.14423 − 1)

= $80.88 / 0.14423

= $560.80/month

Result: Saving $561/month for 3 years, starting with $3,000, reaches the $25,000 goal at 4.5% APY.

Goal: $100,000 college fund in 18 years Starting Balance: $10,000 Annual Rate: 5.0%

r/n = 0.004167

(1.004167)^216 = 2.4540

Part 1 growth: 10,000 × 2.4540 = $24,540

Remaining needed: $100,000 − $24,540 = $75,460

PMT = $75,460 × 0.004167 / (2.4540 − 1)

= $314.40 / 1.4540

= $216.23/month

Result: Starting with $10,000 and contributing $217/month for 18 years at 5% reaches the $100,000 college fund goal.

Savings Calculator in Excel and Google Sheets

The built-in FV function in Excel and Google Sheets handles the complete savings calculation formula:

=FV(rate, nper, pmt, [pv], [type])

Where:

- rate = interest rate per period (annual rate ÷ n)

- nper = total number of periods (years × n)

- pmt = payment per period (enter as negative for outflows)

- pv = present value / starting balance (enter as negative)

- type = 0 for end-of-period payments (default), 1 for beginning-of-period

Example: $10,000 starting balance, $300/month, 4.5% annual rate, 5 years, monthly compounding:

=FV(0.045/12, 60, -300, -10000, 0)

Returns: $30,540.06

Solving for Required Monthly Payment (PMT function)

=PMT(rate, nper, pv, [fv], [type])

Example: How much to save monthly to reach $50,000 in 5 years starting from $5,000 at 4.5%?

=PMT(0.045/12, 60, -5000, 50000, 0)

Returns: -$627.59 (negative indicates cash outflow — you pay $627.59/month)

Solving for Time Required (NPER function)

=NPER(rate, pmt, pv, [fv], [type])

Example: How long to save $30,000 with $400/month at 4.5%, starting from $2,000?

=NPER(0.045/12, -400, -2000, 30000, 0)

Returns: 59.4 periods → approximately 5 years

Common Savings Calculator Mistakes

Mistake 1: Confusing APR and APY

Inputting an APY as if it were an APR and then specifying monthly compounding double-counts the compounding effect, overstating the projected balance. Use APY with n=1, or APR with the appropriate n.

Mistake 2: Ignoring Inflation

A savings calculator projects nominal future value — the number of dollars you will have. It does not account for inflation eroding the purchasing power of those dollars. At 3% annual inflation, $67,000 in 5 years has roughly the same purchasing power as $57,800 today. For long-term goals, always compare your projected savings rate against expected inflation.

Mistake 3: Assuming a Fixed Rate for Variable Accounts

High-yield savings account rates fluctuate with Federal Reserve policy. A rate of 5.0% today may be 2.0% in three years. For multi-year projections, use a conservative blended rate assumption rather than today’s rate applied to the full time horizon.

Mistake 4: Forgetting Taxes on Interest

Interest earned in taxable savings accounts is taxed as ordinary income in the year it is earned. The savings calculator returns a pre-tax figure. In a 22% federal tax bracket, $1,000 of interest income costs $220 in federal taxes, reducing net earnings. For accurate after-tax projections, multiply interest earned by (1 − marginal tax rate).

Mistake 5: Not Accounting for Contribution Increases Over Time

Most savings calculators assume a fixed monthly contribution. In reality, contributions often increase as income grows. A calculator that allows step-up contributions — increasing the monthly deposit by a fixed percentage each year — produces a more realistic long-term projection.

Frequently Asked Questions

How does a savings calculator work?

A savings calculator applies the compound interest formula to a starting balance and regular contributions over a defined time period, projecting the future value of the savings. It accounts for the frequency of compounding (monthly, quarterly, daily) and the annual interest rate to show how money grows over time.

What is the formula for savings calculation?

The complete formula is: FV = P × (1 + r/n)^(n×t) + PMT × [((1 + r/n)^(n×t) − 1) / (r/n)], where P = principal, r = annual rate, n = compounding periods per year, t = years, and PMT = regular contribution per period.

How much will $10,000 grow in 10 years?

At 4.5% compounded monthly with no additional contributions: approximately $15,614. At 5.0%: approximately $16,470. At 7.0%: approximately $20,097. The rate and compounding frequency determine the outcome.

What is the difference between APR and APY in savings?

APR is the base annual rate before compounding. APY is the effective annual rate after compounding is applied. Bank savings accounts advertise APY. Use APY with annual compounding (n=1) or convert back to APR for use in the full compound interest formula.

How much should I save per month?

The required monthly savings depends on your goal amount, time horizon, starting balance, and expected interest rate. A savings calculator solves for the monthly payment directly given the other variables.

Does compound interest really make a big difference?

Yes, especially over long time horizons. On a $10,000 investment at 5% for 30 years, the difference between simple interest ($15,000) and monthly compounding ($22,279) is over $7,000 — from the same principal and rate, with zero additional contributions.

How do I calculate savings interest in Excel?

Use the FV function: =FV(annual_rate/12, years×12, -monthly_contribution, -starting_balance, 0). The result is the projected future balance. For required monthly savings, use the PMT function.

What savings account type offers the best return?

As a general rule, high-yield savings accounts (HYSAs) and certificates of deposit (CDs) offer the highest guaranteed returns among FDIC-insured savings products. I-Bonds offer inflation protection. Returns vary with market conditions and Federal Reserve policy.

Conclusion

A savings calculator is the clearest possible argument for starting today rather than tomorrow. The formula behind it — compound interest applied to regular contributions over time — is one of the few mathematical relationships in personal finance that genuinely rewards patience and consistency above all else. The rate matters. The starting balance matters. But nothing matters more than time.

Run the numbers for your own goals. Input your actual starting balance, your realistic monthly contribution, the best rate you can find, and your target date. The result is not just a projected balance — it is a concrete, mathematically grounded plan that turns an abstract intention into a specific monthly action.

The most important number in any savings calculator is not the future value at the bottom. It is the monthly contribution you commit to — and start — today.

Related Topics

- Interest Calculator: Formula, Examples, and How It Works

- Finance Math Explained: Common Money Formulas With Examples

- Interest Rate Calculator: Formula, Examples, and How It Works

- Retirement Savings Explained (Growth + Withdrawals + Examples)

- Compound Interest Explained: APY, Compounding Frequency, and Practical Examples